Double Tax Deduction for Internationalisation

Companies planning to expand overseas can benefit from the DTDi tax deduction scheme with a 200% tax deduction on eligible expenses for international market expansion and investment development activities

Companies planning to expand overseas can benefit from the DTDi tax deduction scheme with a 200% tax deduction on eligible expenses for international market expansion and investment development activities

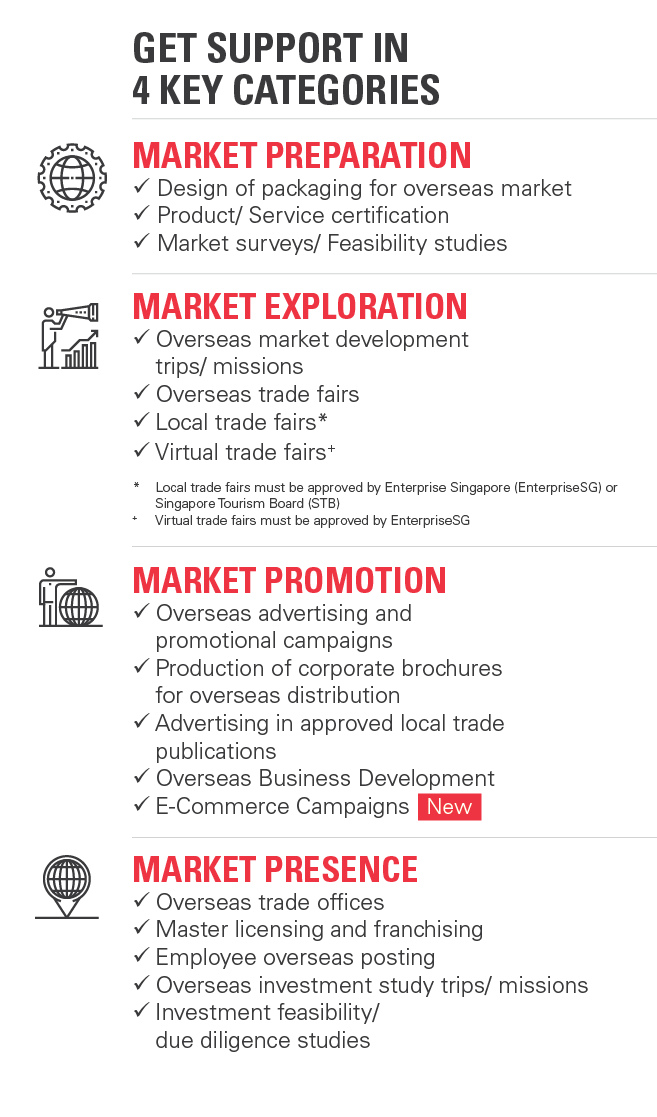

DTDi supports activities across key stages of a company's overseas growth journey

DTDi supports activities across key stages of a company's overseas growth journey

About this programme

Companies planning to expand overseas can benefit from the Double Tax Deduction Scheme for Internationalisation (DTDi), with a 200% tax deduction on eligible expenses for international market expansion and investment development activities.

-

DTDi supports activities across key stages of a company's overseas growth journey, including:

DTDi supports activities across key stages of a company's overseas growth journey, including:

Please refer here for a full list of qualifying activities and expenditure available for DTDi. Employee overseas posting will be subsumed under the Overseas trade office from 1 January 2026. Companies applying for salaries of Singaporean/ Singaporean Permanent Resident posted overseas (previously supported under Employee overseas posting) should submit their application under Overseas trade office form.

Please refer here for the list of approved local trade publications, list of approved virtual trade fairs and the list of standards and certifications approved by EnterpriseSG.

Automatic DTDi

With effect from Year of Assessment 2027, you can claim 200% tax deduction on the first S$400,000 of eligible expenses for all activities (except for “Overseas Trade Office” and “E-Commence Campaigns” when filing your tax returns with IRAS. The cap of $400,000 is applied on a per company basis, regardless of the number of DTDi activities claimed.The activities covered under the automatic DTDi are as follows.

- Overseas Market Development Trip/Mission

- Overseas Investment Study Trip/Mission*

- Overseas Trade Fair

- Local Trade Fair

- Virtual Trade Fair

- Market Survey/Feasibility Study

- Investment Feasibility/Due Diligence Study*

- Design of Packaging for Overseas Markets

- Product/Service Certification

- Overseas Advertising & Promotional Campaign

- Master Licensing & Franchising

- Production of Corporate Brochures for Overseas Distribution

- Advertising in Approved Local Trade Publication

- Overseas Business Development

Please ensure that the expenses are qualifying for the activities before filing for the claims. IRAS reserves the rights to review and request for documentary evidence to substantiate the claims.

Eligibility

-

Business entity resides in Singapore with a primary purpose of promoting the trade of goods or provision of services

-

Businesses enjoying discretionary incentives¹ may also be allowed to qualify for the DTDi scheme on a case-by-case basis, subject to approval by EnterpriseSG or the Singapore Tourism Board

- Incentivised businesses must have their global headquarters in Singapore, with the primary purpose of trading in goods or providing services, and have an intention to internationalise.

-

Project must meet the following key objectives:

- Promotes the company's new products and services to new target market(s)

- Identifies new customers in target market(s) for the company’s existing products and services

- Promotes the company’s new products and services to existing customers

- Promotes the company’s existing products and services to existing markets so as to increase market share

-

Applications must be submitted on the DTDi portal prior to starting the project.

Benefits of DTDi

The examples below illustrate potential tax savings through DTDi when an eligible expense is not an Allowable Business Expense¹ under the Income Tax.

Case 1: Company A spent S$10,000 to participate in an overseas tradeshow to reach out to its buyers in Europe

| Without DTDi support | With DTDi support | |

| Revenue | S$100,000 | S$100,000 |

| DTDi eligible expense of S$10,000 | (S$10,000) | (S$20,000) |

| Other expenses | (S$20,000) | (S$20,000) |

| Taxable income | S$70,000 | S$60,000 |

| Tax payable (@ 17% as of YA2015) | S$11,900 | S$10,200 |

| Savings from DTDi | N.A. | $1,700 |

Case 2: Company B posts a staff into an overseas subsidiary to drive its marketing efforts in-market. Staff basic salary is $2,000 per month.

| Without DTDi support | With DTDi support | |

| Revenue | S$100,000 | S$100,000 |

| DTDi eligible expense of S$2,000 x 12 months | N.A. |

(S$48,000) |

| Other expenses | (S$20,000) | (S$20,000) |

| Taxable income | S$80,000 | S$32,000 |

| Tax payable (@ 17% as of YA2015) | S$13,600 | S$5,440 |

| Savings from DTDi | N.A. | $8,160 |

How to apply

- that do not fall under automatic DTDi

- with quantum exceeding the first S$150,000 for that year of assessment under automatic DTDi

Applications must be submitted before project commencement.

IRAS will assess if expenses submitted qualify for tax deductions.

View the detailed DTDi ESIMS Userguide here.

Need additional help?

Double Tax Deduction for Internationalisation

Other ways we help

Market Readiness Assistance (MRA) Grant

Support for business development, promotion and set-up costs for new overseas market expansion.